Anúncios

In today’s competitive financial landscape, securing a loan with favorable interest rates can significantly impact your long-term financial health.

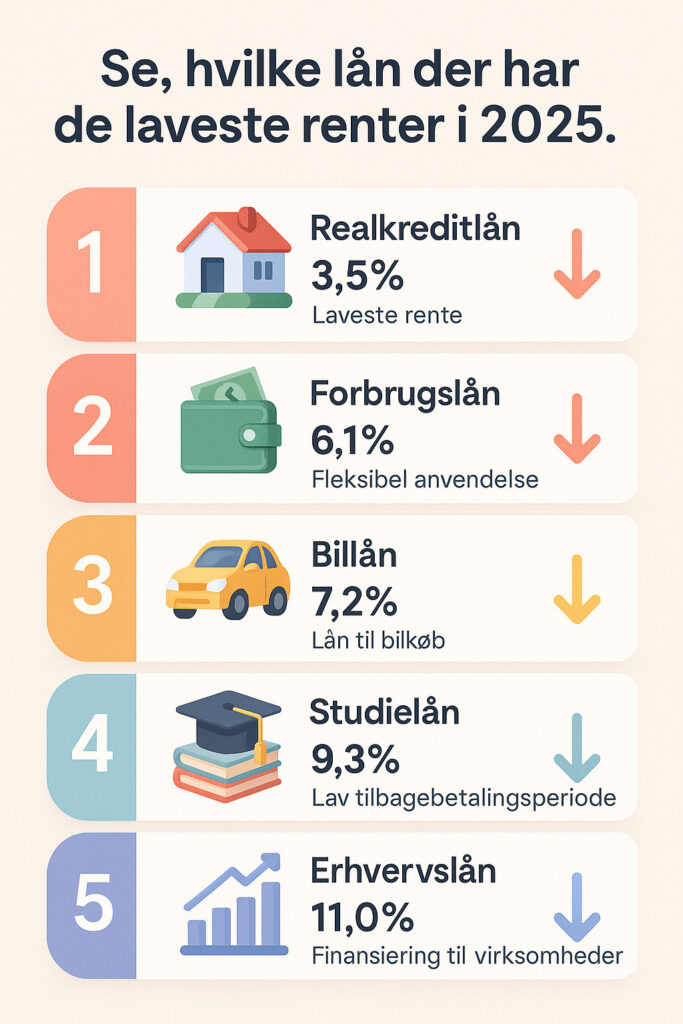

Whether you’re looking to purchase a home, finance education, or consolidate debt, finding the lowest possible interest rate should be a priority. This article examines the top five loans currently offering the most competitive rates in 2025, comparing features, requirements, and potential savings.

Why Interest Rates Matter More Than Ever

With economic fluctuations and central bank policies continuously evolving, interest rates have become increasingly important in loan decisions. Even a 0.5% difference in interest rate can translate to thousands saved over the life of a loan.

For example, on a 2 million currency home loan with a 30-year term, a 0.5% lower interest rate can save approximately 170,000 in total interest payments.

Let’s explore the five loan products currently offering the most competitive rates.

1. Nykredit 30-Year Fixed Rate Mortgage

Key Features:

Nykredit’s 30-year fixed rate mortgage stands out as one of the most stable and affordable long-term financing options in the market.

• Current Interest Rate: 2.85% fixed for entire 30-year term

• Loan-to-Value Ratio: Up to 80% of property value

Anúncios

• Administration Fee: 0.5% of loan amount

• Early Repayment Option: Yes, with favorable terms during market rate fluctuations

• Special Eligibility: Available for both primary residences and investment properties

What Makes It Special:

The unique bond-based mortgage system allows for exceptional stability. When market interest rates rise, borrowers with these fixed-rate loans can actually benefit by buying back their own debt at discounted prices. This system provides a hedge against future interest rate increases that few other global mortgage systems offer.

Best For:

Long-term homeowners who value predictability in their housing costs and want protection against future interest rate increases. Particularly valuable for properties in Copenhagen and other high-growth urban areas where property values continue to appreciate.

2. Danske Bank Green Home Loan

Key Features:

Danske Bank’s Green Home Loan rewards energy-efficient homes with preferential interest rates.

• Current Interest Rate: 2.65% (variable)

• Loan-to-Value Ratio: Up to 75% of property value

• Administration Fee: 0.4% of loan amount

• Energy Rating Requirement: Property must have energy rating of A or B

• Term Options: 10-30 years

What Makes It Special:

Besides the attractive interest rate, borrowers receive a comprehensive energy efficiency assessment and recommendations for further improvements. The bank also offers additional discounts for implementing recommended energy upgrades during the loan term, potentially reducing the rate by another 0.2%.

Best For:

Environmentally conscious homebuyers purchasing new construction or recently renovated properties. This loan is especially attractive for those buying in newer developments in areas like Ørestad or Nordhavn.

3. Nordea Premium Flexible Loan

Key Features:

Nordea’s Premium Flexible Loan combines competitive rates with exceptional flexibility for borrowers with strong financial profiles.

• Current Interest Rate: 3.05% (initial fixed period of 5 years, then variable)

• Loan-to-Value Ratio: Up to 75% of property value

• Interest-Only Option: Available for up to 10 years

• Repayment Flexibility: Allows payment holidays up to twice per year

• Premium Requirement: Total banking relationship of at least 750,000 or monthly income above 45,000

What Makes It Special:

This loan stands out for its flexibility in repayment options and the ability to switch between fixed and variable rates at predetermined intervals. Premium customers also receive personal banking advisors and preferential exchange rates for international transfers.

Best For:

High-income professionals with variable income streams, such as those working in consulting, entrepreneurship, or commission-based industries. The ability to adjust payments provides valuable breathing room during income fluctuations.

4. Realkredit Danmark FlexLife®

Key Features:

Realkredit Danmark’s innovative FlexLife® product provides unprecedented control over loan parameters.

• Current Interest Rate: Starting at 2.95% (variable)

• Loan-to-Value Ratio: Up to 75% of property value

• Unique Feature: Borrowers can adjust their monthly payment, interest-only period, and loan term throughout the life of the loan

• Maximum Term: 30 years

• Special Requirements: Property must be valued at minimum 500,000

What Makes It Special:

Unlike traditional mortgages with fixed parameters, FlexLife® allows borrowers to customize their loan as their life circumstances change. For example, you could reduce monthly payments during parental leave or when financing children’s education, then increase payments when receiving bonuses or inheritance.

Best For:

Homeowners expecting significant life changes in the coming years, including family planning, career transitions, or approaching retirement. Particularly valuable for those with variable income or those who prioritize financial flexibility.

5. Jyske Bank First-Time Homebuyer Loan

Key Features:

Jyske Bank offers a specialized product for first-time homebuyers with exceptionally favorable terms.

• Current Interest Rate: 2.75% fixed for first 5 years, then variable

• Loan-to-Value Ratio: Up to 95% for first-time buyers (combined with a top-up loan)

• Reduced Fees: 50% discount on standard establishment fees

• Age Requirement: Applicants must be under 40 years old

• Educational Requirement: Complimentary housing economy course required

What Makes It Special:

This product combines the traditional mortgage with a top-up loan, allowing first-time buyers to enter the housing market with a smaller down payment. The educational component helps new homeowners understand the responsibilities and economics of homeownership.

Best For:

Young professionals and families purchasing their first home, particularly those with strong income but limited savings for down payment. The educational component is especially valuable for those unfamiliar with the unique property ownership system.

Comparative Overview

| Loan Provider | Interest Rate | Loan Type | Special Features |

|---|---|---|---|

| Nykredit | 2.85% (fixed) | 30-year fixed mortgage | Bond-based system with repurchase option |

| Danske Bank | 2.65% (variable) | Green home loan | Discounts for energy-efficient properties |

| Nordea | 3.05% (5yr fixed, then variable) | Premium flexible loan | Payment holidays and term flexibility |

| Realkredit Danmark | 2.95% (variable) | FlexLife® | Adjustable parameters throughout loan term |

| Jyske Bank | 2.75% (5yr fixed, then variable) | First-time buyer | Higher LTV and reduced fees |

Factors That Affect Your Personal Rate

While these loans offer the lowest headline rates available, the actual rate you receive will depend on several factors:

Credit History and Payment Behavior

Your record in the RKI (credit registry) and payment history with existing debts significantly impact available rates. Maintaining a clean credit history for at least 3-5 years is essential for accessing the best rates.

Employment Stability and Income Level

Lenders favor applicants with stable employment history (minimum 6-12 months in current position) and sufficient income to comfortably cover loan payments. Government employees often receive preferential rates due to their job stability.

Loan-to-Value Ratio

The percentage of the property value you’re financing affects your rate. Lower LTV ratios (more equity) generally secure better rates. For optimal rates, aim for at least 20% down payment.

Property Type and Location

Rates vary based on property type (single-family homes vs. apartments) and location. Urban properties in stable markets like Copenhagen, Aarhus, and Odense typically qualify for better rates than rural properties.

Total Banking Relationship

Many lenders offer relationship discounts when you maintain multiple accounts or services. Consolidating your banking with one institution can reduce your loan rate by 0.1-0.3%.

How to Apply for These Low-Rate Loans

Securing these competitive rates requires careful preparation and approach:

1. Check your credit standing

Request your credit report from the central credit registry to ensure there are no unexpected negative marks. Address any issues before applying.

2. Organize financial documentation

Prepare the last 3 months of pay stubs, annual tax returns for the past 2 years, statements for all bank accounts and investments, and documentation of any existing debts.

3. Calculate your debt-to-income ratio

Lenders typically prefer that your total monthly debt payments (including the new loan) not exceed 40% of your gross monthly income.

4. Get pre-approved

Before property hunting, seek pre-approval to understand your budget and strengthen your position when making offers.

5. Compare total loan costs, not just interest rates

Consider establishment fees, ongoing administration fees, and insurance requirements when comparing the total cost of different loan options.

Real Example: The Jensen Family’s Savings

The Jensen family was looking to purchase a 3.2 million home in a suburban neighborhood. They compared several loan options:

• Traditional Variable Rate Mortgage: 3.4% interest, 30-year term, total interest paid: 1,934,000

• Nykredit 30-Year Fixed: 2.85% interest, 30-year term, total interest paid: 1,587,000

By choosing the Nykredit option, they saved 347,000 in interest over the loan’s lifetime—enough to fund their children’s education or substantially upgrade their retirement savings.

Additionally, when interest rates temporarily spiked to 4.5% three years later, they were protected by their fixed rate while gaining the option to buy back their mortgage bonds at a discount, effectively reducing their outstanding loan balance.

Frequently Asked Questions

Can foreign residents access these low-rate loans?

Yes, but additional requirements apply. Foreign residents typically need at least 2 years of residency, a permanent CPR number, stable employment history within the country, and sometimes a larger down payment (25-30% versus 20% for citizens). Nordea and Danske Bank offer specialized services for international professionals.

How often can I refinance if interest rates drop further?

There’s no legal limit to refinancing frequency, but transaction costs make it impractical to refinance for small rate decreases. As a rule of thumb, a minimum 0.5% interest rate reduction justifies refinancing costs for most loan sizes. Some lenders offer “refinance guarantees” that reduce costs for subsequent refinancing.

Do these low rates apply to second homes or investment properties?

Yes, but typically with a 0.2-0.5% rate premium and stricter equity requirements (minimum 30-40% down payment). Nykredit and Realkredit Danmark offer the most competitive investment property packages, especially for properties in major urban centers.

What happens if interest rates rise dramatically in the future?

Fixed-rate mortgages provide complete protection against rising rates. For variable-rate products, most lenders offer rate caps or the option to convert to fixed rates for a fee. The unique bond-based mortgage system actually creates an opportunity during rising rates, as borrowers can repurchase their mortgage bonds at discounted market values.

Are interest-only options still available with these low rates?

Yes, most lenders offer interest-only periods, typically for up to 10 years. However, choosing this option usually adds 0.1-0.3% to the interest rate and requires higher equity in the property (minimum 25-30% down payment). Realkredit Danmark’s FlexLife® offers the most flexible interest-only options.

Conclusion

The current low-interest environment presents exceptional opportunities for borrowers, but navigating the options requires careful consideration of your specific financial situation and long-term goals. The five loan products highlighted in this article represent the most competitive offerings in today’s market, each with unique advantages for different borrower profiles.

While the headline interest rate is important, remember to consider the total cost of borrowing, including fees, terms, and flexibility. The best loan isn’t always the one with the absolute lowest rate, but rather the one that best fits your individual circumstances and provides the right balance of cost, security, and flexibility.

Before making a final decision, consider consulting with an independent financial advisor who can provide personalized recommendations based on your complete financial picture, not just the loan itself.